Switzerland has a unique tax regime designed to encourage wealthy individuals to move to the country, establishing it as their tax domicile. This is specially helpful for companies or professionals moving to Switzerland as part of an expansion strategy because it allows local workers to streamline their tax payments.

Lump sum taxation essentially taxes individuals based on their annual living expenses rather than their foreign income.

Individuals who benefit from lump-sum taxation are assessed based on their expenses around the world and can even negotiate the tax rate with the Swiss authorities.

While there are specified rules and minimum tax requirements, these tax regulations actively promote moving to Switzerland to enjoy lower tax rates on a variety of income sources.

This includes income from retirement funds, dividends, rental income, and more.

Interested in learning more about lump-sum taxation? Here’s what you need to know to streamline your entry into Switzerland.

Tired of scrolling? Download a PDF version for easier offline reading and sharing with coworkers

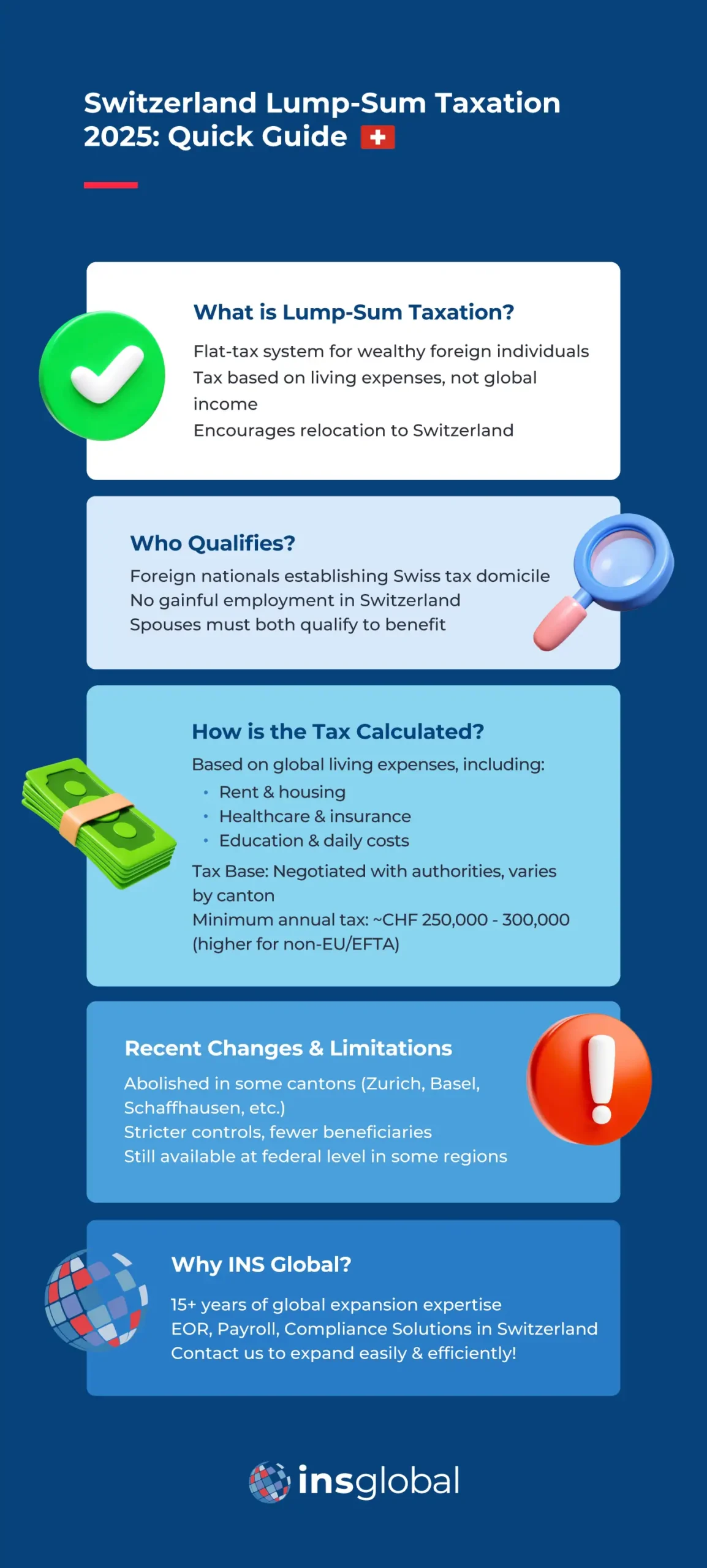

What Is Lump-Sum Taxation?

Lump-sum taxation, also known as the “forfait fiscal,” is a unique tax regime in Switzerland designed to attract foreign nationals to establish their tax domicile in the country. Under this system, eligible individuals, including foreign nationals and Swiss citizens returning after a minimum of 10 years abroad, can opt for a simplified method of assessing their income and wealth for tax purposes. To qualify, they must refrain from engaging in gainful employment within Switzerland.

Instead of taxing their worldwide income and assets, lump-sum taxpayers are assessed based on their annual living expenses in Switzerland and abroad, covering themselves and their dependents.

This approach considers various expenditures such as rent, healthcare, education, and insurance premiums, among others. The tax authorities may negotiate the specific tax base with the taxpayer, and ordinary tax rates are applied to this negotiated base.

While the rules and minimum tax requirements can vary by canton, in practice, the minimum annual tax burden often starts at around CHF 250,000 to CHF 300,000 for non-EU/EFTA nationals. EU/EFTA nationals may enjoy lower tax bases. Additionally, Swiss Social Security contributions are typically required.

Lump-sum taxation offers a simplified and potentially cost-effective tax option for eligible individuals looking to establish their tax residence in Switzerland, provided they meet the necessary criteria and refrain from gainful employment within the country.

What Do I Need to Apply for Lump-Sum Taxation?

To apply for lump-sum taxation in Switzerland, individuals must meet specific criteria and follow a set of requirements outlined by Swiss tax authorities. Here are the key prerequisites and steps to initiate the application process:

Residency Status

Applicants must not have Swiss citizenship and should establish their tax domicile in Switzerland for the first time or after a minimum of ten years spent outside the country.

Lack of Gainful Employment

To qualify, applicants must refrain from engaging in any form of gainful employment within Switzerland. This includes both regular employment and self-employment activities. However, gainful activities outside Switzerland may be permissible, subject to specific regulations.

Spousal Consideration

Spouses living in a legal marriage must each fulfill the above-mentioned requirements individually to benefit from lump sum taxation. If only one party qualifies, then the other will be recognized as a tax resident and be subject to income tax.

Calculation of Tax Base

Tax authorities calculate the tax base on the total worldwide annual cost of living expenses for the applicant and their dependents. This includes various expenditures like housing costs, healthcare, education, and insurance premiums. The specific tax base is typically subject to negotiation with the tax authorities.

Ordinary Tax Rates

Once the tax base is determined, ordinary tax rates are applied. These rates may vary by canton, so it’s essential to consider the specific canton’s regulations.

Minimum Tax Burden

In practice, the minimum annual tax burden for lump sum taxation varies depending on the canton of residence. It generally starts at approximately CHF 250,000 to CHF 300,000 for non-EU/EFTA nationals. EU/EFTA nationals may enjoy more favorable tax bases.

Social Security Contributions

Applicants must make Swiss Social Security contributions of around CHF 25,000 per person annually. This is based on the average rate in Switzerland and can change each fiscal year. While it’s true that not every Swiss person contributes CHF 25,000 every year, this rate applies to individuals who fully support themselves and dependents in Switzerland.

Recent Changes to Lum-Sum Taxation

Lump-sum taxation has come under fire increasingly in recent years, due to the way it provides benefits for wealthy foreigners but deprives Switzerland of tax revenue.

As a result, it has been abolished in several Cantons, including Basel Landschaft, Basel Stadt, Zurich, Schaffhausen, and Appenzell Ausserrhoden. However, because of federal laws, lump-sum taxation can still be applied for federal income tax in these areas.

Overall, there is a sense that lump-sum taxation in Switzerland is facing stricter controls and scrutiny, according to official figures, the number of those benefitting from it has decreased.

However, more and more foreign citizens are moving to Switzerland, so time will tell whether this tax regime continues in its current form.

As always, it’s best to remain vigilant and up-to-date when considering tax regulations. Working with legal and financial professionals to make the most of lump-sum taxation in Switzerland and similar tax liability rules in other countries can help keep you and your workers safe during periods of expansion.

Enjoy the Benefits of Local Tax Advantages by Partnering with INS Global

When it comes to navigating the international market, INS Global has the experience and expertise needed to guide you in Switzerlandd and 100+ countries.

Whether you’re looking to move your business abroad or expand into new markets, INS Global’s international services can help you navigate even the most complex of labor and tax regulations.

Tax regulations when living in Switzerland can get incredibly complicated, a problem made worse if you are unfamiliar with local rules or lack the right local resources.

This is what makes having the right partner so important both when making the decisions and executing them with extreme precision.

For more than 15 years, INS Global has been providing companies with simple and streamlined ways to expand worldwide.

Today we offer tech-forward recruitment, Employer of Record (EOR) in Switzerland, payroll, and compliance assurance solutions so you can explore your options and grow in a way that suits your needs. For companies looking to expand into key neighboring markets, we also provide Employer of Record in Germany to support compliant hiring and rapid operational setup.

INS Global provides the expertise and experience to deal with all the challenges of international expansion. Contact our professional advisors today to learn more about how you can expand quickly, easily, and fearlessly.

FAQ

Which Cantons in Switzerland have lump-sum taxation regimes?

Lump-sum taxation in Switzerland is not uniform across all cantons. Within Switzerland, the level of total tax benefits can vary from one region to another.

The most notable cantons known for their lump sum taxation regimes include Geneva, Vaud, Valais, and Ticino. These cantons have been popular choices for foreign nationals seeking this tax arrangement due to their relatively lower tax burdens and favorable living conditions.

Are lump sum citizens subject to Swiss Social Security?

Lump-sum taxpayers in Switzerland are typically subject to Swiss Social Security contributions, which are around CHF 25,000 per person per year. This is an important point for individuals applying for lump sum taxation, as it forms part of the overall system of tax laws in Switzerland.

What tax treaties exist in Switzerland to avoid double taxation?

Switzerland has an extensive network of tax treaties, also known as double taxation agreements (DTAs), with many countries to avoid double taxation of income and help build cross-border trade and investment.

These treaties cover various types of income, including dividends, interest, royalties, and capital gains. Some of Switzerland’s important treaty partners include Germany, the United States, France, the United Kingdom, and many other European and non-European nations.

Can I switch from lump-sum taxation to regular taxation?

Yes, you can switch to normal tax rules at any time if you no longer meet the criteria or if it becomes more efficient to do so. However, consult with your local tax authorities or a legal professional for details before you make any decisions.

Are there any drawbacks to lump-sum taxation?

One potential drawback is that you are generally unable to engage in gainful work in Switzerland while part of the lump-sum tax regime . At the same time, it may not be the best tax deduction option for those with large worldwide incomes.

How is the total possible amount of expenses applicable for lump-sum taxation determined?

Lump-sum taxable amounts are typically based on the taxpayer’s annual expenses in Switzerland. This figure can vary from one canton to another, but it is usually several times the average Swiss rent for similar areas.

What expenses are considered for lump-sum taxation?

Eligible living expenses typically include things like housing costs, health insurance premiums, education costs, and day-to-day living expenses.

SHARE