- SOLUTIONS

-

- Countries

- Stories

- About Us

-

-

- HOW CAN WE HELP?

- Find out how we can assist you to achieve higher growth through services that are tailored to your company needs.

-

- GLOBAL INSIGHTS

Our PEO Spain service, otherwise known as a global Employer of Record (EOR), works in Spain as your local partner and assists you as you expand into a new market. Our PEO allows your business to outsource its HR services when entering the Spanish market without the need to create a distinct legal entity.

Like an international EOR, a PEO (Professional Employer Organization) provides companies with a way to simply and securely expand their operations overseas by outsourcing critical HR services to a third-party provider like INS Global. With a PEO in Spain, companies can office compliance assurance to employees worldwide in less than 72 hours.

When businesses need support throughout the global expansion process, an Employer of Record (EOR) in Spain offers cost-effective utility by taking care of employer responsibilities. Hire or transfer employees in markets worldwide in a fraction of the time of traditional methods with INS Global’s innovative employment outsourcing solution.

A PEO can offer proficiency in local regulations and accurate best practices for local administrative procedures that keep your company in constant legal compliance.

Estimated time for Company Incorporation in Spain: 4-12 months

Estimated time to establish a PEO in Spain: 5 days

A PEO will provide payroll outsourcing in Spain alongside recruitment and compliance management services. When your company isn‘t spending valuable time on these issues, you can focus on growth.

When entering into a new market, like Spain, simple HR mistakes might lead to a disproportionate occurrence of fees and fines that slow your business down. A PEO will reduce these risks, decrease market entry time, and save money.

Everything your business could need can be provided by one point of contact. This decreases risks and gives you personalized, custom solutions.

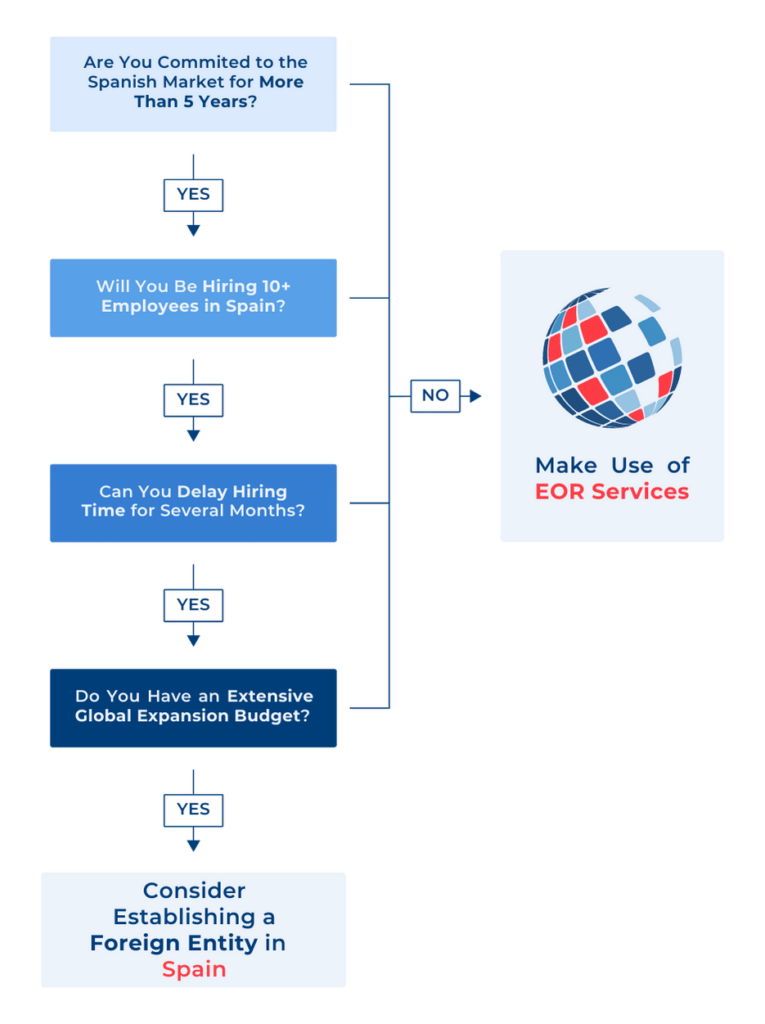

Incorporating your company in Spain can be an excessively complex, risky, and time-consuming process. It often requires a deep understanding of local regulations and the rules for establishing a physical entity within the country. Our PEO in Spain will allow you to operate your business without going through numerous confusing steps required to incorporate a new legal entity.

The Advantage in Figures

| PEO/EOR | Company Incorporation | ||

|---|---|---|---|

|

|

|||

|

Price |

80% Less Expensive |

|

|

|

Market Entry |

2-5 Days |

6 Months |

|

|

Employee Turnover |

Decrease by 14% |

|

|

|

Recommendation |

98% of the Current PEO Clients |

|

|

|

Administrative Fees |

Saves an Average of $450 |

|

|

|

Costly Payroll and Compliance Fines |

Help Avoid |

|

|

|

Company Growth Rate |

7 - 9% |

|

|

|

ROI |

27% |

|

|

|

Closed During Pandemic |

-58% |

|

|

|

|

|

||

Manuel Ramos

TERAO ASIA

Managing Director

We think INS Global is a good solution about starting business in new and complex markets. Understanding the market doesn’t mean you need to set up a company immediately.

INS Global’s PEO can manage employee recruitment and assignment needs in Spain in 4 steps:

Once you‘ve decided to expand into the Spanish market, choosing between PEO and Employer of Record services can seem confusing. It‘s necessary to understand their unique differences so that you can be fully informed and make the best decision for your company.

A PEO is a separate business that outsources HR services to employees working at other companies.

These outsourced services can include payroll outsourcing, tax filings, and consulting on legal regulation compliance.

An EOR is a separate business that acts similarly to a PEO, but it will also maintain legal liability for hiring employees on behalf of other companies.

With a PEO agreement, the employment contract between your company and the employee remains.

With an EOR agreement, the employment contract is directed by your company but legally made between the EOR and your employee.

INS Global provides both PEO and EOR services in Spain to meet your demand. Contact us today to learn more about which service might be best for you.

In general, Spanish Labor Legislation allows for the freedom of form whenever creating a new employment contract. Contracts may be made verbally or in writing. However, either party reserves the right to demand an agreement in writing.

Employment contracts are presumed to be for an indefinite duration. However, there are a limited amount of definite-term employment arrangements in Spain. Once the employee has worked past the original term of a temporary agreement, the relationship will be considered indefinite. The employee will then be entitled to standard severance upon termination. Also, you may be aware of the Special Expat Tax Regime (SETR) for foreign employees when wanting to expand to Spain or attract top personnel for an established company there. Known as “Beckham Law“.

For companies willing to enter the Spanish market and begin operations, understanding the generally applicable labor laws on working hours and public holidays is advantageous.

The maximum legal working hours per day in Spain is 9 hours, to a total of 40 hours per week. The calculation of these working hours is an average calculated annually, which means that the working hours may be distributed irregularly throughout the year as long as this is stated in the employment contract and the employee still receives rest periods.

Employees are entitled to a paid annual leave of at least 30 days per year. Additionally, all employees are entitled to 14 paid public holidays every year.

The official public holidays recognized throughout all of Spain are:

In addition to these national public holidays, there are an additional 4 public holidays that vary according to different regions in the country. Finally, each municipality in Spain determines 2 local public holidays.

Employees in Spain can be eligible for up to a full year of paid sick leave via social insurance. This leave can even be extended to 18 months under special circumstances.

Once they receive proof of incapacity from a doctor, the employer is responsible for paying for the initial period of sick leave allowance. After that, all costs are paid by social security. In these cases, it is the responsibility of the employer to apply for leave allowance on behalf of the employee.

Sick leave allowance is calculated as:

As of 2021, parental leave is now 16 weeks for both parents paid for through Social Security.

6 weeks of parental leave must be taken immediately following the birth, and the remaining 10 weeks can be taken at any time during the first 12 months.

The general corporate income tax (CIT) in Spain is 25%. Other taxes may be applicable, depending on the type of company and the type of business. Resident companies in Spain are taxed on their worldwide income. For PEs (Permanent Establishments) in Spain of foreign companies, NRIT (non-resident income tax) will be chargeable on any income allocated to the PE at a rate of 25%.

In Spain, both employee and employer must make contributions to Spain’s social insurances alongside paying taxes.

These contributions are Social Security (for health-related issues), Unemployment Insurance, and Professional Training.

The following table details the rates of social contributions required for certain businesses operating in Spain:

| Employer Rate | Wages Rate | Total |

Social security: health | 23.60% | 4.70% | 28.30% |

Unemployment insurance | 5.50% | 1.55% | 7.05% |

Guarantee fund for employees | 0.20% | – | 0.20% |

Vocational training | 0.60% | 0.10% | 0.70% |

Total | 29.90% | 6.35% | 36.25% |

Occupational accident | Variable (between 0.90 and 7.30%) | – |

|

Personal income is taxed progressively using the following brackets:

Sub Title Slider 4

VIEW DETAILS

Sub Title Slider 3

VIEW DETAILS

Sub Title Slider 1

VIEW DETAILS

A top-notch PEO in Spain can be your partner in managing all pertinent HR tasks, including payroll, contract administration, and ensuring tax compliance, for a single monthly fee depending on the wages of your co-employed personnel.

Absolutely, EORs give you a safe, convenient, and legal way to move or hire employees in Spain. When you take the time to build your own company structure, this job option also functions permanently.

Absolutely, an EOR can hire employees on your behalf across Spain and internationally.

Indirect costs like social insurance contributions and any bonuses or incentives must also be met by the company in addition to paying new recruits’ salaries. While they are unusual, signing incentives might help you stand out to potential employers.

There can be a minimum or maximum number of employees you can hire while using the services of some PEO companies. INS Global, nevertheless, enables you to oversee as many or as few staff as your development strategy necessitates.

Our recruiting professionals have access to professional networks and offline and online resources for the business and are knowledgeable about local norms and best practices.

A professional staffing firm or recruitment agency will often charge a recruiting fee in Spain that is determined as a percentage of the new hire’s monthly gross salary. These services may be provided by INS Global, who can also completely integrate them with our PEO system to provide a comprehensive employment outsourcing package.

Absolutely, both Spanish nationals and international residents may use INS Global’s recruiting, PEO, and EOR services.

Spanish employees are paid every month. Those employees working with a CBA (which includes a large number of Spanish workers) may also receive additional paychecks in January and December.

Each paycheck must clearly show all income details, as well as all deductions for taxes and social security contributions.

Currently, the Spanish minimum wage is €1,080 gross per month over 14 months (due to most workers receiving 2 bonus paychecks per year; the monthly minimum wage worked out over 12 months comes to €1,260).

In Spain, employers are in charge of handling all payroll taxes, benefits administration, and workplace safety to at least the minimum standards as written in the labor code and all relevant regulations.

Acts allowing employees new rights have recently been approved in Spain, including the freedom to work from home and the ability to refrain from responding to work-related emails after hours. The employer is required to ensure compliance with all of these as well as any other laws or regulations.

Alongside managing tax deductions and payments on behalf of employees each payroll period, employers have to organize social security contributions. In Spain, social security payments are based on gross salary; they amount to up to 6% for the employee and 31% for the employer.

This may involve applying relevant deductibles like the so-called “Beckham Law”.

Spanish employment legislation covers the minimum salary, maternity and paternity leave, paid time off, overtime, illness, retirement, and insurance. Transport help, discounts, and any advantages that a business may desire to provide in order to attract potential workers are examples of fringe benefits.

Small changes may be made without requiring an employee’s consent, but larger changes must be made after negotiation. It’s still considered best practice to have the employees informed consent to all changes, however small.

In addition, recent regulations have been passed aiming to reduce the use of temporary or limited contracts.

The majority of primary healthcare in Spain with free with residents only being required to pay a percentage of prescription medications.

Or every year of service with a company, an employee can expect 20 days of salary as severance pay (up to a maximum equivalent to 12 months) A 15 minimum notice period may be ignored if the employer pays the employee for this time.

No, in fact thanks to recent changes to the law, remote work is now fully integrated into Spain’s labor law. Remote employees must have all the same rights as office workers. Additionally, changes to visa laws mean that employees working in Spain for less than 3 years may apply for a remote work visa.

The Ministry of Labor ensures the most comprehensive list of regulations concerning labor in Spain. This document is known as the Workers’ Statute (Estatuto de los Trabajadores).

Spain’s public holidays are heavily dependent on the region that an employee works in. They vary between 10-18 days and are paid at the rate of a standard workday unless the employee is required to work.

Level 39, Marina Bay

Financial Centre Tower 2,

10 Marina Boulevard

Singapore 018983